Welcome to Irrigation & Lighting magazine’s first Green Industry Outlook Survey. This year’s 2022 survey builds on the trends from past years, reaching back to 2019 and giving us an even sharper focus on the changes the industry has faced over time. With four years of data to work with, we can trace these lines with greater accuracy.

While we’ve referred to past surveys to help us build a better understanding of the wider industry, this year’s survey brings several changes to the table. First, it boasts the most respondents we’ve ever had, bringing in a total of 1,583. Of those, more than half are industry contractors, providing a close-up look at the day-to-day challenges and opportunities for growth. Even with a larger number of participants, the data correlates well with past years, giving us even more assurance that we’re getting real results from the professionals who are doing the work in the field. Once again, we’re so grateful for the help of our readers in developing this outlook every year, bringing in differing perspectives from all angles.

Next, we’ve added questions specific to both irrigation and landscape lighting professionals. These will help develop a picture of what each of these market segments looks like in the wider market. In some cases, we’ve broken out results of more general questions with responses just from irrigation and lighting professionals to provide additional insight.

Regardless of what part of the industry you were in, last year was a challenge for one reason or another. Some felt the pressure from the pandemic to find ways to keep the lights on. For many, it was a struggle to find the capacity to cover current customers alongside those who suddenly had new ideas about how to improve their outdoor spaces thanks to more time spent at home.

Our survey followed readers as they looked at what could’ve been a year of economic strain turn into multiple opportunities for growth. It tracked changing demographic trends as they’ve slightly shifted toward newcomers, and business expectations as they neatly flipped from last year’s. We continued our research on important issues such as crew diversity, and added more business benchmarking questions that cover topics such as minimum job costs and marketing efforts.

Once again, we’d like to thank Heritage Landscape Supply Group for sponsoring this project for the second year running. This year, Heritage provided a DJI Mini 2 quadcopter and a Solo Stove Bonfire fire pit as the two drawing prizes for completing the survey.

If you’re looking ahead at the new year while trying to capitalize on new expansion opportunities or looking for where your company fits alongside your colleagues, our report will help you get above the landscape for a clear view. Use these results to build your best plan for the upcoming year.

An industry in focus

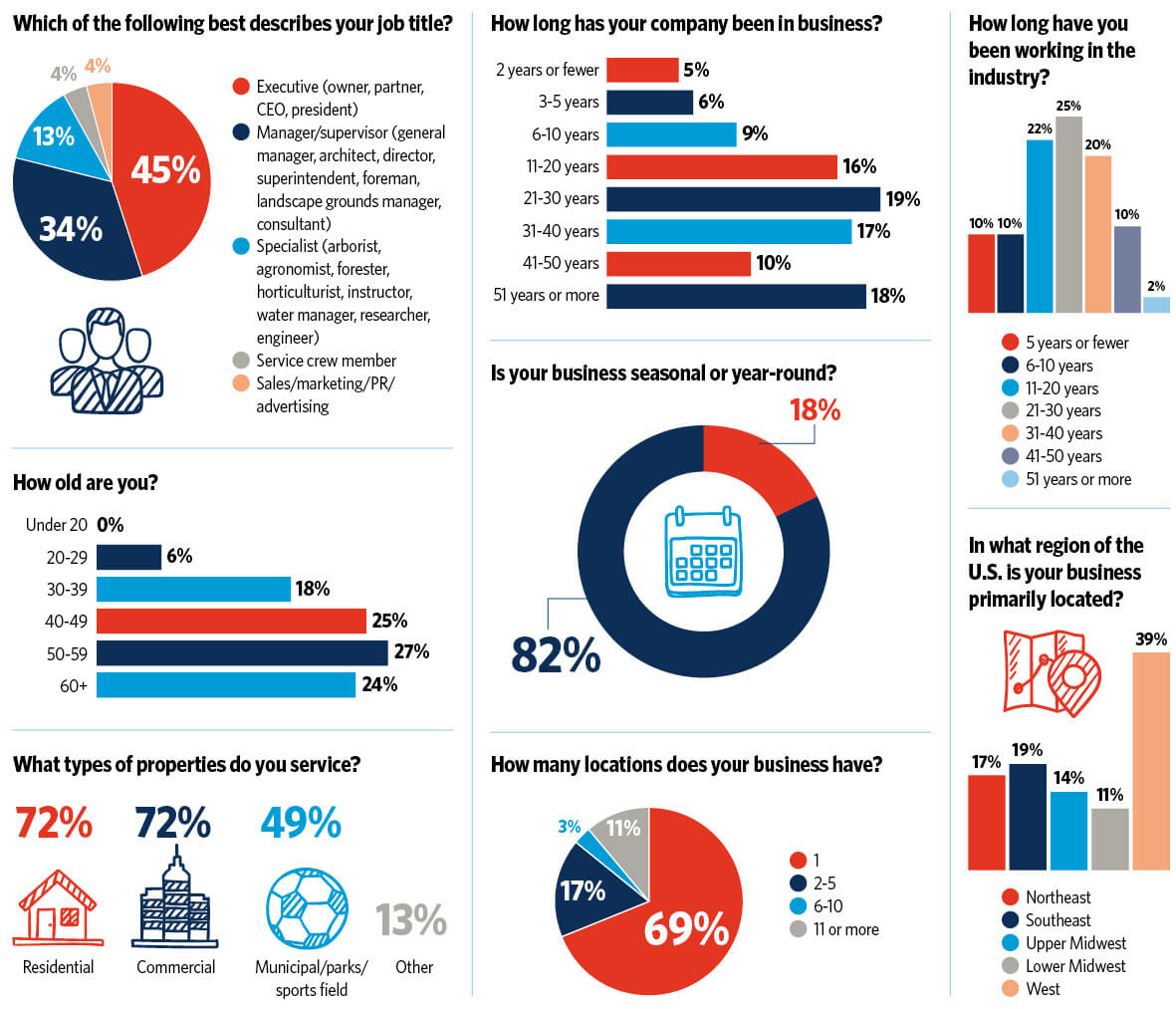

Even with more respondents than ever, our survey’s demographic breakdown is similar to the past four years’ reports. Starting with distribution countrywide, the West still accounts for the majority of the green industry (39%). The East Coast makes up exactly the same amount as last year’s survey (36%) to come in second, with the Upper Midwest continuing to decline in favor of the Lower Midwest.

The number of businesses that operate year-round has only dropped a single point over the past four years (82%), compared to seasonal services. It looks as though the number of companies picking up new work in the past year didn’t convince many to switch to an all-year model.

Contractors still make up the majority of survey respondents, totaling 63% compared to any of the others. One interesting change this year is that irrigation contractors (30%) picked up the lead from landscape contractors (22%), alternating positions from last year’s results. The next three results, including government and municipality workers (10%), landscape architects (9%) and lawn care contractors (7%), also maintained their hold in the top five from last year.

The majority of respondents overall are executives (44%) and managers (34%), continuing a slow trend over the last few surveys seeing more distribution between the two. Also a growing trend is the number of respondents who consider themselves to be specialists more than anything else, with 12% this year compared to 7% last year and 4% the year before. For those respondents who are contractors, almost everyone works as the executive (60%) or manager (28%).

Survey respondents still boast plenty of industry experience, with 33% having worked personally in the green industry for more than 31 years, dropping only mildly from last year’s 37%, but also on a downward trend from 2020’s 42%. That could line up with a shift toward industry newcomers, as the next biggest change was for respondents with five years of experience or fewer, up to 10% from 7% last year.

After shifting slightly last year, respondents’ age ranges stayed mostly the same, with some mild additions to those between 30 and 39 years old and between 50 and 59 years old.

In keeping with last year, half of the companies are family owned (50%), though that’s down slightly from last year (55%) and continuing down from 2019’s high of 63%. Privately held companies (34%) are at about the same as last year’s report (32%). Government representatives are on an upswing (15%), continuing a climb from 2020’s 8%.

Pushing for growth

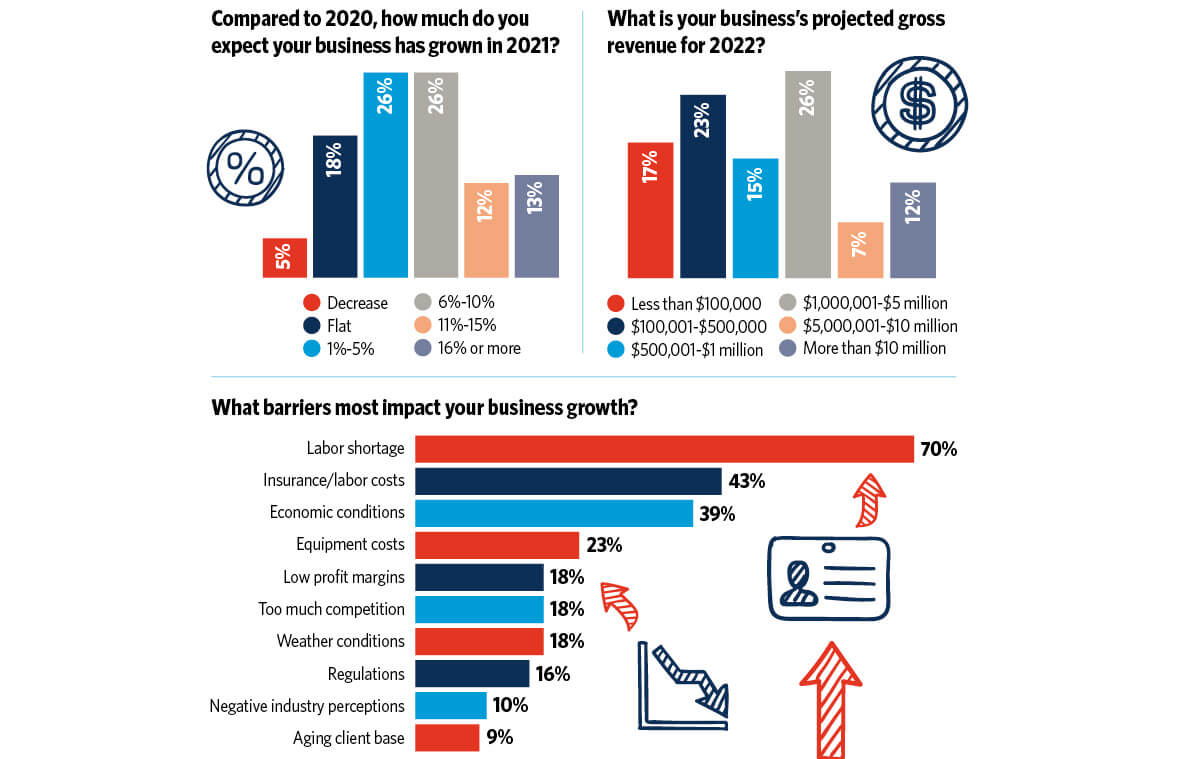

Green industry business owners are a generally more optimistic group than they were a year ago. It’s tough not to be, given the amount of work that rushed the market thanks to COVID-19 keeping so many people at home and thinking of ways to improve their living spaces. On estimated growth from the past year, responses are almost completely flipped from the previous survey. A full 52% have grown between 1% and 10%, and a quarter (25%) are looking at an increase of 11% or more. Contractor respondents were even more enthusiastic, with 30% expecting that same increase. These numbers fall more in line with 2020 and 2021, showing that last year was something of an outlier for a lot of numerous reasons.

Perhaps as evidence of the belief that business will remain stable, projected gross revenues for the year stayed roughly the same as each previous year of the survey. Most respondents expect to land in the same brackets, between $100,001 and $500,000 (23%) or between $1,000,001 and $5 million (26%).

Looking at what held businesses back from achieving their best growth, respondents cited a labor shortage (70%) as far and away the biggest hurdle. It accounted for almost the next two, insurance and labor costs (43%) and economic conditions (39%), combined. A total of 80% of contractor respondents said a labor shortage was their worst challenge in the past year. Though labor has been the top concern for the past three years of the survey, this year seemed like an especially tough block to deal with for professionals.

Getting good help

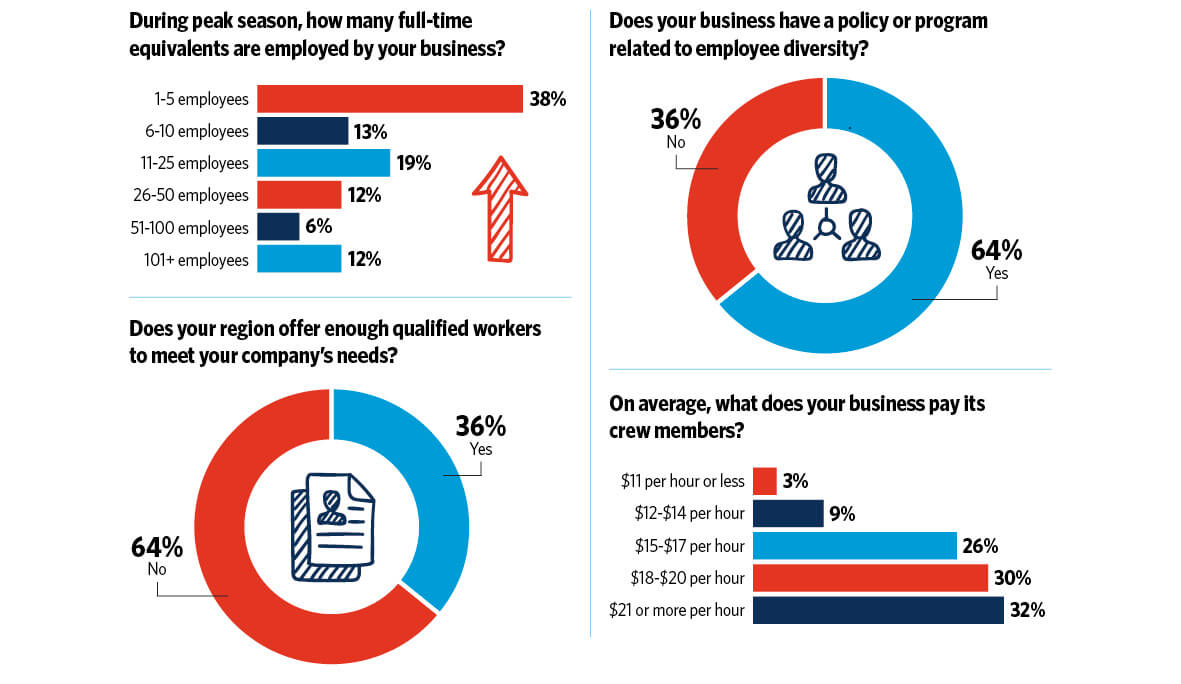

Green industry professionals fought to bring in new employees and develop the current team in the past year to try to get the most out of the work coming in. But doing so wasn’t easy for everyone. For the fourth year running within a difference of just two points, almost the exact same number of respondents (64%) say their region doesn’t have enough qualified workers to support their needs. Contractor respondents were even more dire, with almost three quarters (73%) saying there weren’t enough hands to do the work.

That said, the total number of full-time employees during peak season hasn’t meaningfully shifted by more than a few points in any category in the past three years, suggesting that overall crew sizes have remained about the same for many, even with the extra jobs available.

Breaking down the survey responses regarding labor, a few different smaller trends emerge. Employers who say they can find enough employees tended to respond that they have more racially and gender-diverse companies, and have a policy or program related to encouraging employee diversity. It’s not uncommon for prospective employees to look for people who look and sound like them at a company before they apply. There was no meaningful variance between the two groups when it came to encouraging training and certification.

Another difference between them came in how much crew members are paid on average. Those who say they can find enough crew members more often paid $18 per hour or more. That’s compared to those who say they can’t, who more often paid between $15 and $20 per hour. That could be part of the reason that those who can’t find enough workers more often increased average crew member pay in the past year. Interestingly, that group also offers monetary bonuses or incentives more often, by a difference of almost 10%. At least in the current market, potential employees could be looking more for a reliable paycheck than possible bonuses.

Opportunities ahead

While more general landscape contractors picked up a lot of work in the past year, those providing irrigation or landscape lighting services still had plenty of reasons to be excited. Irrigation and lighting professionals both projected about the same gross revenue as overall green industry professionals for the past year. With just a few points of difference, they also have roughly the same expectations for how their businesses have grown in the past year.

Irrigation contractors tend to find their customer leads more frequently through business partner referrals (14%) as compared to direct market outreach (11%), where lighting contractors have those two reversed. All contractors tend to rely on customer referral vastly more (67%) than anything else, however.

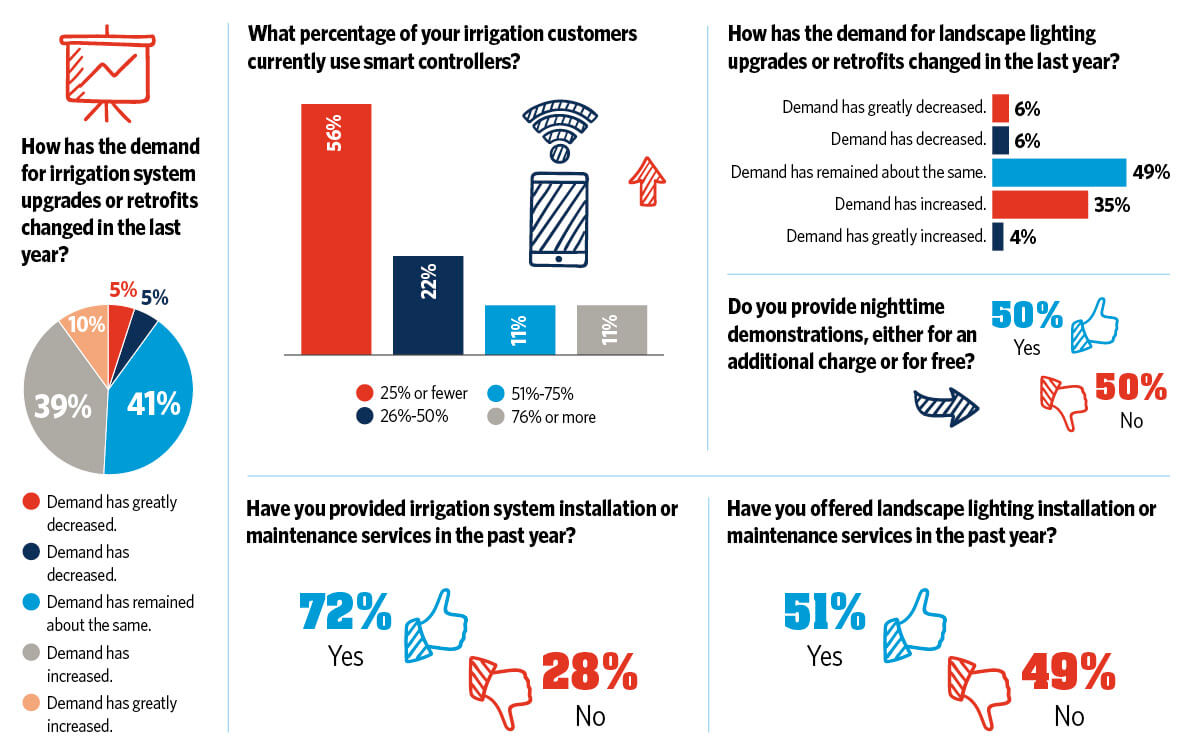

In the past year, almost half (49%) of irrigation contractors have generally seen an increase in system upgrades and retrofits. On the landscape lighting side, those seeing an increase in upgrades looks more like 39% total. While many new clients last year were looking for ways to improve their existing landscapes and systems, it seems like there’s still availability left in the market for both segments.

Another potential opportunity for irrigation contractors to make an impact is through smart controllers. As more states enact regulations on responsible water usage, it’s likely to become an even easier sell to discuss subjects like pressure regulation and smart controllers. More than half (56%) of irrigation contractors say their customers use a smart controller with their system, meaning there’s still plenty of ground to cover.

One of the practices that landscape lighting contractors use to differentiate themselves, nighttime demonstrations, provides an additional point of contention. Among those contractors, the survey is neatly split, with 50% on each side saying they do or don’t provide them, whether for an additional charge or free. There’s no denying the visual impact of a customer seeing their property lit at night, but it seems there’s an equal number of contractors showing that effect through previous work or modeling apps and keeping their evening hours free.

Looking up

All things considered, it looks like the contractors who were so optimistic last year ended up a little more accurate from this vantage point. This year, a total of 91% of green industry professionals are still expecting moderate to significant growth. That’s up from even last year’s 88%, and from 79% the year before. Irrigation-focused trends swept the top three of the those expected to increase in the next year, with smart irrigation technologies (49%), remote irrigation system management (28%) and native/low water landscaping (27%).

Overall, respondents are looking forward to a year of growth after a year of stress and uncertainty.

“Increased time at home over the past couple years has reminded clients about the need for attractive outdoor spaces they can enjoy,” writes a respondent.

Technology and an increase in customer awareness of smart water practices have had an effect as well, whether that awareness came as a result of state regulation or not.

“There is a renewed interest in smart and environmentally friendly options,” writes another. “The technology is catching up with expectations and is available/affordable for the average customer.”

But for many professionals, unlocking that expected growth is dependent on solving the labor puzzle, as has been the case for many years in the industry’s past.

“Demand is at an all-time high,” writes a respondent. “If I could find the employees, we could grow at a rapid rate. Right now, we have to limit the amount of work we take on due to our capacity.”

Methodology

The 2022 Green Industry Outlook Survey was developed in SurveyMonkey with three email invitations including individual, anonymous links sent to respondents between Nov. 18 and Dec. 10, 2021. Responses gathered were checked for duplicates and relevance to the survey. Each invitation included information on the drawings for a DJI Mini 2 quadcopter drone or a Solo Stove Bonfire fire pit, provided by Heritage Landscape Supply Group. Survey results were closed Dec. 10 with 1,583 responses. Irrigation & Lighting staff analyzed the survey results.